The Paper Shield: PF & ESIC Challans vs Real Compliance Risk | EHSSaral

Labour Law Compliance Compliance Governance EHS Leadership PF Compliance ESIC Compliance Principal Employer Liability Contractor Management

Last updated:

|27 Apr 2026

Read time: 15 min read

Why Collecting PF & ESIC Challans Is Not the Same as Verifying Compliance

The Compliance Illusion in Contractor Management

Why documents feel like protection

In most Indian factories, contractor bill clearance follows a well-rehearsed routine.

A PF challan is attached.

An ESIC challan is attached.

HR signs off.

Finance releases the payment.

The file looks complete.

Registers are updated.

Everyone moves on.

From the outside, compliance appears “done”.

This belief - that document collection equals compliance - is deeply embedded in how organisations operate. It is not laziness. It is habit, built over years when paperwork was the system of record.

And for long stretches of time, this approach works.

Until one day, it doesn’t.

When the illusion collapses

A large automotive component manufacturer received an EPFO notice in 2024 for contractor dues from 2021–2023. The contractor had wound down operations in 2022. Internal files showed 42 challans, all approved. EPFO records showed 23 actual deposits. The gap? HR had verified formats. Finance had cleared bills. But no one had checked backend credits. The exposure: ₹38 lakhs + penalties

The illusion rarely breaks during normal operations.

It breaks under pressure.

- When a workplace accident happens and an ESIC card is rejected at the hospital

- When a retrospective audit asks for proof of deposits from two or three years ago

- When an inspector asks a quiet but decisive question:

“Was the money actually credited?”

At that moment, organisations realise something unsettling:

The challans were checked.

But the deposits were never verified.

This is not a story about incompetence or bad intent.

It is a story about systems mistaking paperwork for proof.

The Legal & Governance Reality for Principal Employers

Joint liability is not theoretical

For a mid-sized contractor with 200 workers, unpaid PF/ESIC dues + penalties can easily exceed ₹15–20 lakhs. If the gap spans three years and includes interest, exposure climbs to ₹40–50 lakhs or more. And by the time the notice arrives, the contractor is often unreachable - but the liability is on your desk.

Under Indian labour laws, responsibility is structured clearly:

- Contractors are required to deposit PF and ESIC contributions

- Principal Employers can be held jointly liable if those deposits never happened

This liability does not disappear because:

- Bills were paid

- Invoices were approved

- Challans were collected and filed

- No irregularity was noticed at the time

From an enforcement perspective, authorities are not concerned with intent.

They are concerned with credit.

Did the money reach the statutory system or not?

If the answer is no, recovery powers extend to the Principal Employer - especially when the contractor is no longer traceable.

This is why liability often surfaces years later, when relationships have ended and memories have faded.

Why EHS & Factory Managers inherit this risk

Many assume PF and ESIC are purely HR or Finance matters.

In practice, the exposure travels differently.

EHS professionals and Factory Managers often:

- Act as the Occupier

- Control contractor access and gate passes

- Represent the site during inspections

- Sign statutory declarations

When compliance gaps surface, enforcement does not chase internal workflows.

It looks for the responsible person at the factory level.

This is why safety professionals and plant heads often inherit liabilities created far away from the shop floor.

Compliance is not departmental.

It is a single ecosystem.

How Invalid Challans Enter “Good” Systems

Common patterns seen across industries

When PF or ESIC issues emerge, the immediate assumption is fraud.

That assumption is usually incomplete.

What is seen far more often are process gaps, not criminal intent.

Some common patterns include:

- Old challans reused with modified months

- TRRN generated, but payment failed or was later reversed

- Partial payments presented as full compliance

- Genuine challans submitted - but linked to a different establishment

From a document perspective, these challans often look perfectly acceptable.

They are stamped.

They are signed.

They match expected formats.

And that is precisely why they pass routine checks.

Why PDFs create false confidence

A challan PDF looks identical whether:

- Payment succeeded

- Payment failed

- Payment was reversed later

- Only part of the amount was credited

Formats do not change.

Visual cues do not warn you.

The document reflects what was intended.

The statutory system reflects what actually happened.

When organisations rely only on PDFs, they are trusting intention - not outcome.

That distinction rarely matters during day-to-day operations.

It matters enormously during audits.

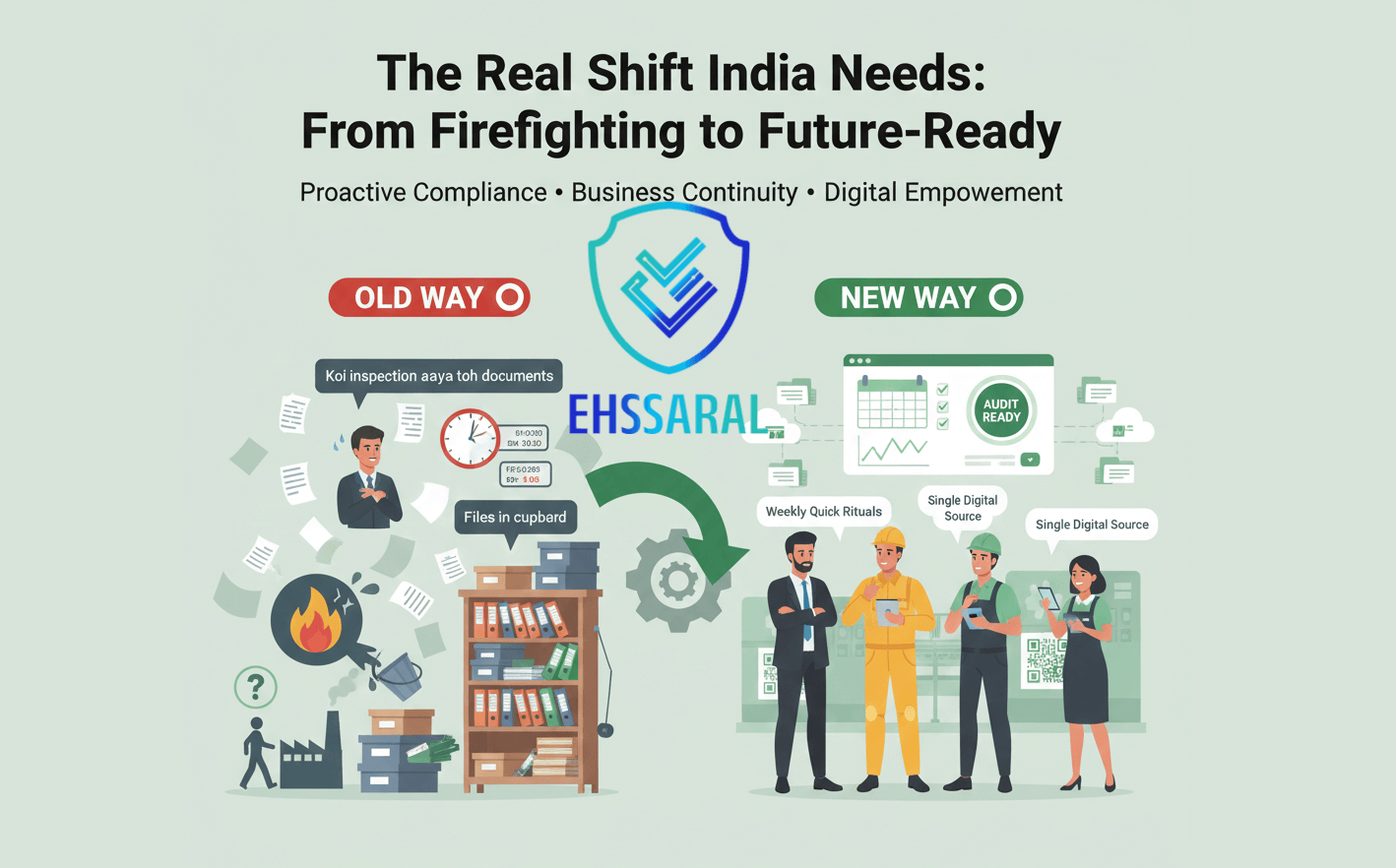

Why This Risk Stays Invisible for Years

Paper-era processes in a digital-era system

Most internal contractor compliance systems were designed when:

- Physical challans were the final proof

- Audits relied heavily on file reviews

- Enforcement was manual and episodic

Over time, statutory systems evolved:

- Backend transaction trails became permanent

- Cross-year data matching became possible

- Digital footprints began to persist indefinitely

What did not evolve at the same pace were internal clearance processes.

As a result, many organisations still operate with paper-era assumptions inside digital-era enforcement systems.

That mismatch is where exposure quietly builds.

Read Why Most Environmental Non-Compliance Is a System Failure, Not Intent by EHSSaral

When enforcement became visible, not stricter

Many professionals feel enforcement has suddenly become harsher.

In reality, it has become more visible.

Modern audits rely less on random sampling and more on:

- Backend data matching

- Retrospective analysis

- Algorithm-driven flags

Digital systems do not forget old periods.

They connect dots silently.

Gaps that went unnoticed earlier are now surfaced automatically - often years after the contractor relationship ended.

Where This Leaves Most Organisations

By this point, most experienced readers reach the same realisation:

“This is not about catching someone wrong.

It’s about whether our systems can prove compliance later.”

That realisation is uncomfortable - but necessary.

Because the biggest risk here is not fraud.

It is false comfort.

And false comfort lasts just long enough to create real liability.

Read more about Decoding the Factories Act 1948 by EHSSaral

Why Checklists and Documents Give False Comfort

Collection is not verification

Most organisations believe they are protected because they follow a checklist.

The checklist typically asks:

- PF challan received

- ESIC challan received

- Wage register attached

- Attendance sheet submitted

From an internal control perspective, this feels sufficient.

But these checklists answer only one question:

“Did we receive a document?”

They do not answer the more important question:

“Can we independently prove this deposit later?”

That distinction is subtle - and critical.

Checklists are designed to ensure collection discipline.

They are not designed to ensure evidence durability.

As long as enforcement relied on manual inspection and physical files, this distinction did not matter much. In a digital enforcement environment, it matters a great deal.

Why standard checklists create false comfort

A checklist gives a sense of closure.

Once boxes are ticked, the file is closed and attention moves elsewhere. That psychological closure is powerful - and misleading.

The problem is not that checklists are wrong.

The problem is that they stop one step too early.

They assume that:

- A challan equals a deposit

- A format equals a transaction

- A file equals proof

Those assumptions are no longer safe.

Where the System of Record Actually Lives

The quiet truth most teams miss

Here is the part that surprises many senior professionals:

The system of record already exists - and much of it is public.

PF and ESIC contributions leave backend trails inside statutory systems. These trails are not created by PDFs. They are created by actual credit events.

Verification does not require:

- Logging into contractor accounts

- OTP access

- Vendor cooperation

It requires knowing where truth lives.

Internal processes were built assuming documents were the final truth.

Statutory systems now operate assuming backend data is the truth.

Those two assumptions are no longer aligned.

EPFO and ESIC maintain transaction-level data tied to TRRNs, ECR filings, and establishment codes. If you know where to look, deposits can be independently traced - without logging into contractor accounts or needing their cooperation.

Why PDFs are weak evidence in audits

A challan PDF is a snapshot of intent.

It tells you:

- What was supposed to happen

- What amount was generated

- What period was covered

It does not reliably tell you:

- Whether payment succeeded

- Whether payment was reversed

- Whether the full amount was credited

From an audit standpoint, this distinction is decisive.

When auditors compare backend records with internal files, they are not judging effort. They are checking outcomes.

That is why organisations with “perfect files” still face exposure.

A TRRN is generated the moment a transaction is initiated - even if payment fails minutes later. The challan PDF looks identical in both cases. Only backend records distinguish success from failure.

Verification as a Mindset, Not a Policing Tool

The wrong fear around verification

Verification often meets resistance because it is misunderstood.

Teams worry that it implies:

- Distrust of contractors

- Extra workload

- Operational delays

In reality, verification is about future-proofing, not fault-finding.

It is not about questioning people.

It is about strengthening systems.

A better internal question to ask

Instead of asking:

“Did we check the challan?”

Ask:

“Can this challan be validated during an audit - without calling the contractor?”

That single question shifts behaviour.

It moves the organisation from:

- Paper completeness

to - Evidence resilience

Verification, when framed this way, becomes a governance function - not a policing activity.

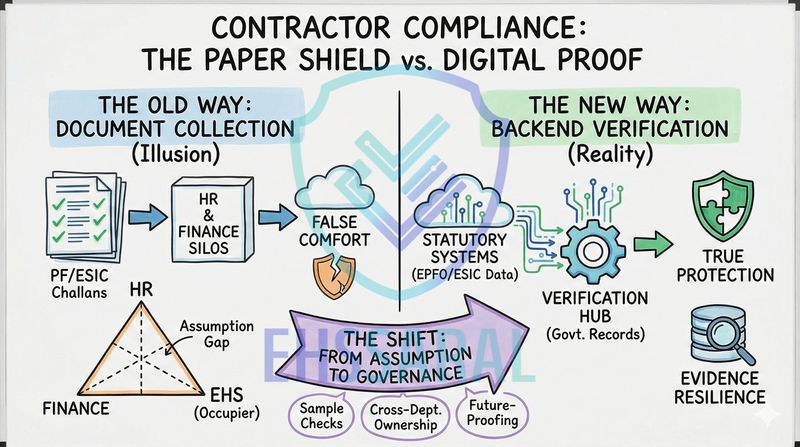

The Assumption Gap Inside Organisations

The HR–Finance–EHS liability triangle

This is where most silent exposure originates.

In many organisations:

- HR collects and stores compliance documents

- Finance clears bills and manages payments

- EHS / Factory Manager (Occupier) carries statutory liability

Each function performs its role sincerely.

But no one owns end-to-end verification.

This creates an assumption loop:

- HR assumes Finance will flag payment issues

- Finance assumes HR verified authenticity

- EHS assumes both systems are reliable

The gap between these assumptions is where exposure hides.

Why the person with liability has the least visibility

This is the structural imbalance most organisations don’t notice.

The Occupier or Factory Manager - the person legally responsible - often:

- Does not see challans

- Does not access payment records

- Does not control document workflows

Yet, when enforcement action arises, accountability travels upward - not sideways.

This is not a people problem.

It is a design problem.

Why This Is a System Failure, Not a People Failure

Good people, weak connections

Most professionals involved in contractor management are:

- Overloaded

- Operating under time pressure

- Managing multiple vendors and sites

Expecting any one person to “catch everything” is unrealistic.

The issue persists because:

- Responsibility is fragmented

- Verification ownership is undefined

- Assumptions replace controls

When no one is explicitly responsible for verification, everyone assumes it is happening somewhere else.

That assumption holds - until it doesn’t.

A Quiet Test Every Organisation Should Pass

Three questions worth asking internally

Without assigning blame, ask:

- Can we verify a challan from six months ago without contacting the contractor?

- Do we retain transaction references in a way that survives staff turnover?

- Can internal audit independently confirm deposits if asked tomorrow?

If two or more answers are “no”, you are not non-compliant.

You are exposed.

The good news is that exposure created by systems can be reduced by systems - once acknowledged.

What This Means for Senior Leadership

For plant heads, EHS leaders, and occupiers, the implication is strategic.

Compliance is no longer about effort or intent.

It is about provability.

Strong organisations are not those with perfect paperwork.

They are those whose systems can answer calmly when questions arise years later.

That calm comes from structure - not memory.

How Mature Organisations Reduce This Risk (Without Distrust)

Organisations that handle this risk well do not become suspicious of contractors.

They become structured.

The shift is subtle but decisive:

- From “collect everything”

- To “verify selectively and consistently”

This is not about checking every challan, every month. That approach is neither practical nor necessary.

What mature organisations typically do instead:

- Sample-based verification

- For example, verifying 10–20% of challans on a rolling basis

- Full verification for higher-risk scenarios

- First-time contractors

- High-value or manpower-heavy vendors

- Contractors with fluctuating headcount

- Separation of records

- Challans are filed

- Verification references are logged independently

This allows organisations to balance trust with diligence - without slowing down operations.

Factory Act & Compliance Thresholds for factory Headcount as per new Labour codes

Why This Is Governance, Not Micromanagement

A common concern raised internally is:

“Won’t this slow down bill clearance?”

In practice, the opposite usually happens.

Clear ownership and defined verification processes:

- Reduce last-minute panic during audits

- Prevent blame-shifting across departments

- Allow senior management to respond calmly to inspectors

Instead of scrambling through old emails or chasing contractors who no longer exist, the organisation knows exactly what can be proven and how.

That confidence is not created by paperwork.

It is created by governance.

Some organizations verify 100% of challans for the first three months of a new contractor relationship, then shift to quarterly sampling for established vendors. Others flag contractors with sudden headcount changes or payment delays for targeted checks.

Why This Risk Will Increase in the Digital Era

Many professionals assume digitisation will make compliance easier and reduce disputes.

Digitisation does simplify processes - but it also increases visibility.

Key shifts already underway:

- Interconnected labour, tax, and financial databases

- Long-term retention of transaction-level data

- Algorithm-driven retrospective audits

- Cross-period analysis covering multiple years

Digital systems do not forget.

They quietly connect historical dots - even when organisations have moved on.

What was once invisible due to fragmented systems is now being surfaced automatically.

This is not stricter enforcement.

It is continuous visibility.

With systems like e-Shram and Unified Labour Portals under development, multi-year, cross-employer compliance trails are becoming the norm - not the exception.

The Digital Footprint Problem

Every PF and ESIC transaction leaves a footprint.

That footprint persists even when:

- Contractors shut down

- Business relationships end

- Staff members change

- Physical files are archived

In earlier years, time diluted exposure.

In the digital era, time amplifies it.

This is why organisations relying solely on document collection often feel blindsided when issues surface years later.

The system remembers what people don’t.

A Quick Self-Assessment for Senior Teams

Without assigning blame, ask honestly:

- Can we verify a six-month-old challan without calling the contractor?

- Do we retain transaction references in a format that survives employee turnover?

- Can an internal audit team independently confirm deposits if asked tomorrow?

If two or more answers are “No”, you are not alone.

Most organisations operate this way.

The difference lies in whether this gap is acknowledged early - or discovered through a notice.

What This Means for EHS & Factory Leadership

For EHS professionals and Factory Managers, this issue is not abstract.

They are often the ones who:

- Sign statutory declarations

- Control contractor access and gate passes

- Represent the site during inspections

When systems fail elsewhere, liability lands at the factory gate.

Understanding this risk does not mean stepping into Finance’s role.

It means ensuring that compliance systems across HR, Finance, and EHS speak the same language - proof, not paper.

Closing Perspective: Proof Over Paper

Most compliance failures are process failures, not intent failures.

The real question is not:

“Did we want to comply?”

The real question is:

“Can our systems prove that we did - years later?”

Paperwork creates comfort.

Proof creates protection.

Organisations that understand this early rarely panic later.

Frequently Asked Questions (FAQs)

1. Is collecting PF and ESIC challans sufficient for compliance?

No. Collecting challans only confirms that a document exists.

Compliance is established only when the actual contribution is credited in the EPFO/ESIC system. Audits focus on deposits, not paperwork.

2. Why is the Principal Employer liable even if the contractor was paid?

Under PF and ESIC laws, the Principal Employer has joint liability if contributions were not deposited - regardless of whether contractor invoices were cleared or challans were submitted.

Payment to the contractor does not transfer statutory responsibility.

3. How do PF/ESIC issues usually surface years later?

Most cases arise during:

- Retrospective audits

- Data-driven backend scrutiny

- Accident-related verification

- Cross-year database matching

Because digital systems retain historical transaction data, gaps from earlier years become visible later.

4. Are fake PF or ESIC challans common?

In many cases, the issue is not deliberate fraud.

More often, challans are:

- Reused

- Generated but not paid

- Partially paid

- Linked to another establishment

They look genuine on paper but do not reflect actual deposits.

5. Why don’t standard contractor compliance checklists catch this risk?

Most checklists are designed for document collection, not backend verification.

They confirm that challans were received - not that money was credited. This creates false comfort until an audit occurs.

6. Can PF or ESIC deposits be verified without contractor login or OTP?

Yes.

EPFO and ESIC maintain transaction-level records that can be independently cross-checked using references such as TRRNs, ECR filings, and establishment details.

Verification does not require access to contractor accounts.

7. Why does this matter to EHS or Factory Managers? Isn’t this an HR/Finance issue?

EHS and Factory Managers often act as the Occupier and represent the site during inspections.

When compliance gaps surface, liability typically lands at the factory level, even if the process failure originated elsewhere.

8. How much financial exposure can arise from PF/ESIC non-deposits?

For a mid-sized contractor (150–200 workers), unpaid dues plus penalties and interest can easily exceed ₹15–20 lakhs for a single year.

If gaps span multiple years, exposure can rise to ₹40–50 lakhs or more.

9. Is 100% verification of challans required to stay compliant?

No.

Many mature organisations follow:

- Sample-based verification (e.g., 10–20%)

- Full checks for high-risk or first-time contractors

The goal is evidence durability, not distrust.

10. Why will this risk increase in the future instead of reducing?

Because compliance enforcement is becoming data-driven.

With interconnected labour databases, long-term transaction storage, and retrospective analytics, gaps that were invisible earlier are now automatically flagged - even years later.

Harshal T Gajare

Founder, EHSSaral

Founder - EHSSaral| Partner - Perfect Pollucon | ISO 14001 Lead Auditor | Second-generation environmental professional simplifying EHS compliance for Indian manufacturers through practical, tech-enabled guidance.

Related Blogs

TSDF Process for Hazardous Waste: What Happens After Dispatch | EHSShala

EHSShala Foundations - Core Environmental Basics for EHS Officers

Other Waste Streams in Indian Factories | Battery, E-Waste, Plastic & More | EHSShala

MPCB Consent Guide: CTE, CTO, Renewal, Fees & Conditions | EHSShala

List, Rules & Compliance Guide ehssaral.webp)

Orange Category Industries in India (2026): List, Rules & Compliance Guide

Environmental Monitoring Guide for Indian Factories: Air, Water & Noise | EHSShala

Evolution of EHS in India - (Part 1) Pre-Bhopal Era | EHSShala

Transforming SME Compliance: Zero Surprise Failures in India | EHSSaral Research