BRSR Core 2026: Why Compliance Automation Is Now Mandatory | EHSSaral

BRSR Core ESG Audits Environmental Compliance Scope 3 Reasonable Assurance Compliance Automation

Last updated:

|7 Feb 2026

Read time: 10 min read

The End of “Good Intentions” Reporting

For years, sustainability reporting in India operated on trust.

If a company disclosed its environmental initiatives, shared broad metrics, and demonstrated intent, that was considered sufficient. CSR narratives, ESG disclosures, and sustainability sections in annual reports focused on what was being done - not always how consistently it was being executed.

That era is ending.

By 2026, environmental responsibility for Indian companies is no longer judged only by declarations or activity lists. It is increasingly evaluated through audit-grade data, traceability, and system-level assurance.

This shift is not philosophical.

It is procedural.

Regulatory expectations around Business Responsibility and Sustainability Reporting (BRSR), particularly BRSR Core, are moving decisively from self-declared compliance to verifiable compliance. What matters now is not just whether environmental actions exist, but whether they can withstand scrutiny - repeatedly, consistently, and across reporting cycles.

In this environment, spreadsheets, email trails, and manual trackers are no longer sufficient.

Automation is no longer a technology upgrade.

It is becoming a compliance prerequisite.

Regulatory Clarity: BRSR vs BRSR Core (In Plain Terms)

BRSR (Business Responsibility and Sustainability Reporting) became mandatory for India’s top listed companies from FY 2022–23, as notified by Securities and Exchange Board of India.

BRSR Core is not a separate law, but a strengthened assurance framework layered on top of BRSR.

What changes under BRSR Core is not what you report -

it is how rigorously that information is examined.

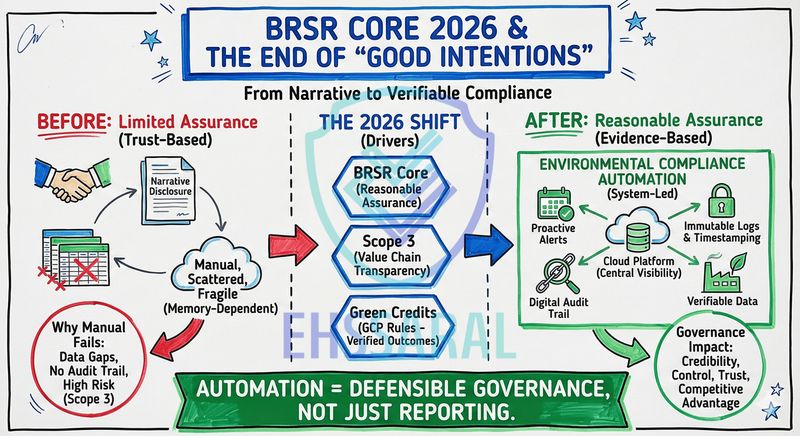

From FY 2026–27 onwards, several BRSR disclosures will shift from Limited Assurance to Reasonable Assurance, making system-backed, audit-grade evidence essential.

In short:

BRSR is mandatory.

BRSR Core makes weak compliance visible.

The 2026 Regulatory Shift That Changes Everything

The most significant change shaping this transition is the move from Limited Assurance to Reasonable Assurance under the BRSR Core framework.

Under Limited Assurance, auditors primarily assessed whether disclosures were plausible and broadly supported. Under Reasonable Assurance, the bar is higher. Auditors are expected to validate:

Data accuracy

Process consistency

Control mechanisms

Evidence trails supporting reported metrics

This shift fundamentally alters how environmental data is evaluated.

Auditors will no longer accept explanations like “the data exists with the plant” or “the consultant manages this.” They will look for system-based evidence - documented processes that demonstrate how data is generated, verified, stored, and retrieved.

For environmental parameters such as emissions, water usage, waste handling, and compliance status, this creates a clear challenge.

Most Indian companies still manage environmental compliance operationally - through plant teams, EHS officers, consultants, and vendors - while reporting expectations are now audit-driven and centralised.

The gap between how compliance is executed and how it is examined is widening.

Read more about CSR Trends 2026: Environmental Compliance Automation in India by EHSSaral

Difference Between BRSR and BRSR Core (What Actually Changed)

Many professionals assume BRSR Core introduced new ESG indicators.

That is not the real shift.

The core difference lies in assurance depth and evidence expectations.

| Aspect | BRSR | BRSR Core |

|---|---|---|

| Applicability | Top listed companies | Same companies, higher scrutiny |

| Nature of disclosure | Narrative + metrics | Metrics + audit-grade evidence |

| Assurance type | Limited Assurance | Reasonable Assurance |

| Auditor focus | Plausibility | Process integrity & controls |

| Tolerance for manual systems | Moderate | Low |

| Risk of qualification | Lower | Higher if controls are weak |

From a compliance standpoint, BRSR asked “What happened?”

BRSR Core asks “How do you know this keeps happening correctly?”

That difference is what makes automation relevant.

Why Manual Compliance Breaks Under Audit Pressure

Environmental compliance, in practice, is inherently fragmented.

Different plants operate under different consents.

Conditions are issued at different times.

Monitoring schedules vary by location.

Records sit with multiple stakeholders.

Under day-to-day operations, this fragmentation is manageable.

Under audit conditions, it becomes fragile.

Reasonable Assurance does not test intent.

It tests repeatability.

If a company cannot consistently demonstrate:

Which consent conditions apply to which unit

Whether monitoring was conducted on schedule

How deviations were identified and corrected

Where records are stored and who owns them

then the issue is no longer environmental performance alone - it is control failure.

This is where many companies will feel pressure in 2026.

Not because pollution suddenly increased.

But because compliance systems did not evolve fast enough.

Why Environmental Compliance Automation Enters the Picture

Environmental compliance automation is often misunderstood as an ESG reporting tool.

In reality, its role is more foundational.

Automation provides a structured backbone that connects regulatory obligations with operational execution and audit verification. It enables:

Central visibility of compliance status across units

Consistent task ownership and timelines

Automated reminders before non-compliance occurs

Traceable documentation aligned to audit expectations

This is not about replacing human judgment. It’s about supporting it with structure.

Most importantly, it creates process memory.

Instead of compliance residing in individuals, inboxes, or vendor files, it resides in a system that can be examined, tested, and trusted.

As audit expectations harden, this distinction becomes critical.

In 2026, the question for Indian companies will no longer be:

“Are we doing the right things?”

It will be:

“Can we prove - consistently - that we are doing them?”

The Value-Chain Test: Why Scope 3 Changes the Conversation

For many large Indian companies, internal environmental compliance is no longer the weakest link.

The real challenge sits outside the factory gate.

Under BRSR Core, companies are now expected to report on Significant Value Chain Partners - typically suppliers or customers that account for a defined portion of purchases or sales. In practice, this pulls environmental accountability into the supply chain, where compliance maturity varies widely.

This is where Scope 3 pressure becomes real.

A listed company may operate with structured systems, trained EHS teams, and documented processes. Its suppliers, however, are often MSMEs operating with:

Limited EHS staff

Heavy dependence on consultants

Manual compliance tracking

Minimal audit preparedness

Yet, environmental non-compliance at a supplier site can still create reputational, operational, and disclosure risks for the principal company.

This creates a difficult position.

Companies are expected to disclose value-chain risks, but they do not directly control supplier operations. They are accountable for visibility, not execution.

The “2% Reality”: Why Manual Tracking Fails at Scale

In theory, Scope 3 disclosures sound manageable.

In practice, even a conservative application of value-chain thresholds can pull 15–30 suppliers into reporting scope - across multiple environmental parameters.

For each supplier, companies may need to understand:

Whether environmental consents are valid

Whether monitoring schedules are being followed

Whether waste handling obligations are met

Whether any notices, deviations, or violations exist

Whether hazardous waste storage and disposal records are complete and traceable

Trying to manage this through emails, declarations, and periodic questionnaires creates three problems:

Data inconsistency – Information arrives in different formats, at different times

Verification gaps – Declarations cannot be independently validated

Audit fragility – Evidence chains break under scrutiny

Manual approaches may work for one cycle.

They rarely survive repeat audits.

This is why Scope 3 compliance is less about collecting data and more about maintaining a verifiable trail.

Why Automation Enables Visibility Without Liability

One concern often raised by companies is whether supporting supplier compliance increases legal responsibility.

This is a valid concern.

Environmental compliance automation addresses this by separating visibility from control.

A system-based approach allows companies to:

View compliance status without managing day-to-day execution

Identify risk patterns without issuing operational instructions

Support preparedness without assuming regulatory responsibility

Automation creates a common language - dates, conditions, records, alerts - without transferring ownership.

For suppliers, it introduces structure.

For principal companies, it introduces clarity.

This balance is difficult to achieve manually.

It becomes feasible when compliance information is systematised.

Why 2026 Is the Breaking Point

The combined effect of Reasonable Assurance and Scope 3 disclosure is cumulative.

Individually, each requirement is manageable.

Together, they create a system stress test.

Companies that rely on informal processes will find themselves answering the same questions repeatedly:

Where is the evidence?

Who verified this?

How do you know this is complete?

Can you reproduce this next year?

These are not environmental questions alone.

They are governance questions.

And governance questions demand systems.

Audit Trails, Not Narratives: What Auditors Will Actually Look For

As BRSR Core moves toward Reasonable Assurance, the nature of audit conversations is changing.

Earlier, sustainability discussions often revolved around narratives:

What initiatives were undertaken

What intent guided decisions

What outcomes were achieved in a given year

Under audit conditions, narratives give way to process evidence.

Auditors will increasingly test whether companies can demonstrate:

How environmental data is generated at the source

How obligations are translated into tasks

How deviations are identified and escalated

How records are stored, retrieved, and protected

How the same process works across sites and over time

This is what an audit trail actually means.

It is not a single document.

It is a chain of repeatable actions.

In mature systems, this evidence trail is supported by system-generated logs and digital timestamping that auditors can test.

When compliance information is scattered across emails, spreadsheets, and third-party files, that chain breaks easily. Under Reasonable Assurance, broken chains translate directly into qualifications, observations, or management letters.

Automation does not “prepare documents for auditors.”

It prepares processes for examination.

Meanwhile, another regulatory development is reinforcing the same principle of verifiable compliance.

What Are BRSR Core Indicators (From an Audit Lens)

BRSR Core indicators are not new ESG ideas.

They are existing environmental and social metrics that now require stronger proof.

From an environmental compliance perspective, auditors focus less on the indicator name and more on whether the following can be demonstrated:

Source-level data generation

Defined responsibility for data capture

Monitoring frequency consistency

Deviation tracking and closure

Record retention across reporting cycles

For example, when reporting on emissions, water usage, or waste handling under BRSR Core, the question is no longer:

“Did this activity occur?”

It becomes:

“Can this data be reproduced, verified, and defended two years later?”

This is why systems - not summaries - determine audit outcomes.

Green Credits and the Shift From Activities to Verifiable Outcomes

Alongside BRSR Core, India’s Green Credit framework is reinforcing the same principle: proof over promise.

Under the Green Credit Programme (GCP) Rules, 2023, Green Credits are not issued for intent.

They are issued for outcomes that survive verification.

Afforestation, water conservation, and ecosystem restoration projects are now expected to demonstrate:

Survival over defined periods

Quality thresholds (such as canopy density)

Ongoing monitoring rather than one-time reporting

This introduces a new challenge for CSR and sustainability teams.

Activities alone are no longer sufficient.

They must be tracked over time.

Manual reporting may capture project initiation.

It struggles to demonstrate sustained performance.

Automation enables continuity:

Periodic monitoring reminders

Data logs across years

Evidence trails aligned to registry expectations

This is not about technology sophistication.

It is about ensuring that good intentions remain verifiable long after the launch event.

Why Prevention Now Outweighs Remediation

Historically, many organisations managed environmental risk reactively.

A notice arrives.

A consultant is engaged.

Documents are assembled.

Operations resume.

Under tightening disclosure and assurance norms, this approach becomes expensive and unreliable.

Reactive compliance leads to:

Higher audit stress

Increased consultant dependency

Last-minute corrections

Reputational exposure

Preventive compliance shifts the equation.

When systems surface obligations early, flag deviations, and maintain records continuously, the cost of compliance stabilises. More importantly, surprises reduce.

From a governance perspective, this matters.

Reasonable Assurance does not penalise honest errors as harshly as it penalises lack of control. Systems demonstrate control. Manual processes rarely do.

The Emerging Divide Among Indian Companies

By 2026, a clear divide is likely to emerge.

On one side:

Companies with structured compliance systems

Consistent audit trails

Repeatable processes across units and suppliers

On the other:

Companies dependent on individuals and vendors

Fragmented records

Compliance that resets every reporting cycle

This divide will not always show up as fines or closures.

This divide is already visible in early assurance exercises, where some companies receive clean reports while others accumulate qualifications-not due to environmental failure, but due to control gaps.

It will appear as:

Auditor discomfort

Qualification notes

Investor questions

Board-level escalations

In this environment, environmental compliance automation is no longer a “nice to have” or an ESG add-on.

It becomes part of how organisations defend credibility.

What This Means for EHS Teams and Plant Managers

In most organisations, BRSR pressure does not land on reporting teams first. It lands on plant teams.

EHS officers are expected to produce audit-grade evidence for obligations they never designed systems to capture. Plant managers are asked to “prove compliance” at short notice, even when records are scattered across vendors, emails, and local files.

This is why 2026 feels heavy. It is not because work suddenly increased. It is because assurance standards changed while compliance tools stayed the same.

Automation is not about adding another layer of reporting. It is about restructuring existing compliance work into a system that can be verified without panic.

BRSR Core Applicability: Who Is Directly Affected?

BRSR Core applies directly to listed entities covered under SEBI’s BRSR mandate.

However, its operational impact extends beyond listed companies.

Why?

Because BRSR Core requires disclosure on Significant Value Chain Partners.

This means:

MSME suppliers may be asked to provide compliance visibility

Environmental records once considered “internal” may now be requested

Audit preparedness expectations travel down the supply chain

In practice, many MSMEs will first encounter BRSR Core not through regulators, but through their customers.

This is where systemised compliance becomes relevant even for non-listed entities.

From Compliance Burden to Competitive Advantage

As regulatory scrutiny increases, environmental compliance is often viewed as a defensive necessity - something to be managed carefully to avoid disruption.

In practice, companies that invest early in structured compliance systems begin to experience a different outcome.

When environmental data is reliable, traceable, and audit-ready:

Board discussions shift from firefighting to oversight

Investor queries become easier to answer

ESG disclosures feel controlled rather than exposed

Internal teams spend less time assembling information and more time analysing it

Compliance stops being episodic.

It becomes continuous.

This distinction matters because, under BRSR Core and related frameworks, credibility compounds. Companies that demonstrate consistent control year after year face fewer questions, fewer escalations, and fewer surprises.

Over time, this translates into trust - not only with regulators, but also with investors, lenders, and global partners.

Why Automation Strengthens Governance, Not Just Reporting

It is important to clarify what environmental compliance automation does not do.

It does not replace regulatory judgment.

It does not eliminate inspections.

It does not guarantee zero violations.

What it does is strengthen governance.

By embedding compliance into daily operations rather than treating it as an annual reporting exercise, automation ensures environmental responsibility isn’t dependent on individual memory, calendar reminders, or last-minute vendor rescue.

Governance frameworks function best when controls are built into the system, not enforced from outside it.

In this sense, compliance automation is less about technology and more about institutional memory - preserving knowledge, obligations, and accountability even as people, vendors, or leadership change.

The Long-Term Implication for Indian Enterprises

As India integrates more deeply into global supply chains and sustainability-linked finance, expectations around environmental discipline will continue to rise.

Access to capital, participation in international markets, and inclusion in responsible investment portfolios increasingly depend on demonstrable control, not declarations.

For Indian enterprises, this creates a strategic choice.

They can continue to manage compliance reactively - assembling narratives each year, relying on individuals, and absorbing audit stress as a cost of doing business.

Or they can build systems that make compliance boring, predictable, and defensible.

The second path does not eliminate regulation.

It makes it survivable.

EHSSaral Insight: Why Most BRSR Core Gaps Are Invisible Until Audit

In our work with Indian plants and compliance teams, we see a consistent pattern:

Most BRSR Core issues are not discovered during operations.

They surface only during assurance reviews.

The reason is simple.

Manual systems hide gaps during routine work.

Audits expose them because they test consistency, not effort.

This is why companies feel “surprised” by qualifications - even when day-to-day compliance felt under control.

Clarity at the process level avoids surprises later.

Closing Perspective

The tightening of BRSR Core requirements is not a sudden shock.

It is the natural outcome of a system maturing.

As environmental responsibility moves from intent to evidence, from disclosure to assurance, and from activities to controls, the role of systems becomes unavoidable.

Environmental compliance automation is not a trend layered onto ESG.

It is the operational backbone that allows ESG commitments to endure scrutiny.

By 2026, Indian companies will not be judged only by what they claim to do.

They will be judged by what their systems can consistently prove.

Frequently Asked Questions (FAQs)

What is BRSR Core and why is 2026 critical for Indian companies?

BRSR Core is the strengthened framework under India’s Business Responsibility and Sustainability Reporting regime that requires assurance-backed ESG disclosures. By FY 2026–27, many listed companies will move from Limited Assurance to Reasonable Assurance, meaning environmental data must be verifiable, repeatable, and system-supported, not just self-declared.

What does “Reasonable Assurance” mean in practical terms?

Reasonable Assurance requires auditors to validate processes and controls, not just outcomes. Companies must demonstrate how environmental data is generated, verified, stored, and reproduced across cycles. Manual spreadsheets and ad-hoc documentation often fail this test because they lack traceability and consistency.

Why is environmental compliance automation becoming non-negotiable under BRSR Core?

Because BRSR Core audits test control maturity, not intent. Environmental compliance automation provides a system-based audit trail-linking consent conditions, monitoring schedules, records, and corrective actions-making compliance defensible under scrutiny year after year.

How does BRSR Core affect Scope 3 and supply-chain disclosures?

BRSR Core expands scrutiny beyond company-owned sites to Significant Value Chain Partners. Companies must now demonstrate visibility into supplier compliance risks. Manual declarations from MSMEs are difficult to verify, whereas system-based compliance tracking enables visibility without operational control.

Will supporting supplier compliance increase legal liability for principal companies?

No. Properly designed compliance systems separate visibility from responsibility. Automation allows companies to identify risk patterns and preparedness levels without managing day-to-day supplier operations or assuming regulatory liability.

Why do many companies fail environmental audits despite good on-ground performance?

Most failures are procedural, not environmental. Common issues include missing documents, unclear task ownership, missed monitoring schedules, and inability to reproduce records during audits. These failures indicate control gaps, which are precisely what Reasonable Assurance audits surface.

How are Green Credits changing CSR and compliance expectations?

Green Credits require long-term verification, not one-time activity reporting. Projects such as afforestation or water conservation must demonstrate survival, quality thresholds, and ongoing monitoring. Automation enables continuous tracking and evidence retention over multiple years.

Is environmental compliance automation only relevant for large listed companies?

No. While BRSR Core applies to listed entities, its impact cascades into MSMEs and suppliers. Companies that rely on MSME supply chains increasingly need structured compliance visibility to meet disclosure and assurance expectations.

Does automation replace consultants or regulatory oversight?

No. Automation strengthens execution and record-keeping. Consultants and regulators continue to play their roles. What changes is that compliance becomes system-supported rather than memory-dependent, reducing last-minute firefighting.

What is the biggest risk of not upgrading compliance systems before 2026?

The risk is not immediate shutdown-it is credibility erosion. This may appear as audit qualifications, investor discomfort, governance escalations, or reduced access to sustainability-linked finance. These risks accumulate quietly but are difficult to reverse once trust is lost.

Is BRSR Core mandatory for all companies?

BRSR Core is mandatory for companies already covered under SEBI’s BRSR framework. However, its impact extends to suppliers and MSMEs through value-chain disclosures, making indirect compliance visibility increasingly necessary.

When did BRSR become mandatory in India?

BRSR became mandatory for the top listed companies in India starting FY 2022–23, replacing the earlier Business Responsibility Report (BRR).

Are BRSR Core formats or templates prescribed?

SEBI has issued BRSR Core formats and annexures outlining indicators and assurance expectations. However, compliance success depends less on templates and more on whether underlying systems can consistently generate verifiable data.

Harshal T Gajare

Founder, EHSSaral

Founder - EHSSaral| Partner - Perfect Pollucon | ISO 14001 Lead Auditor | Second-generation environmental professional simplifying EHS compliance for Indian manufacturers through practical, tech-enabled guidance.

Related Blogs

Chemical Accidents Rules, 1996: A Practical Guide for Indian EHS Officers

Late Filing Penalty for Form 4 SPCB: What Happens If You Miss the 30 June Deadline?

Water & Effluent Sampling Basics for Indian Factories | EHSSHala

EHSShala Foundations - Core Environmental Basics for EHS Officers

ehssaral.webp)

Hazardous Waste Form 4 Portal Errors (MPCB & GPCB Fix Guide)

Guide for Indian Factories EHSShala by EHSSaral.webp)

Ambient Air Quality Monitoring (AAQM) Guide for Indian Factories | EHSShala

Practical Guide for Indian Factories EHSShala.webp)

Hazardous Waste Management Rules (2016) – Practical Guide for Indian Factories | EHSShala

CPCB OCEMS Flatline Notice: How Industries Should Respond (Safely) | EHSSaral