ehssaral.webp)

The Digital Compliance Cliff: EPR Traceability Challenges for Indian MSMEs | EHSSaral Research

Research & Policy EPR Compliance MSME Regulation Environmental Compliance India CPCB Digital Governance Traceability Systems

Last updated:

|2 Feb 2026

Read time: 14 min read

The Digital Compliance Cliff

How Portal-Based Traceability Regimes Are Reshaping MSME Environmental Compliance in India

Author: Harshal T Gajare

Affiliation: Founder, EHSSaral

Date: December 2025

Executive Summary

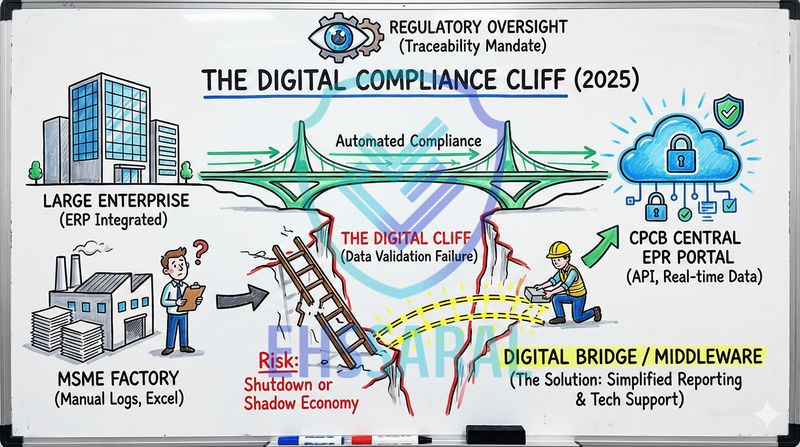

India’s environmental compliance framework has entered a decisive new phase. Between 2023 and 2025, regulatory enforcement has shifted from predominantly physical inspection-based models to portal-mediated, rule-based digital traceability systems. This transition is most visible in the implementation of Extended Producer Responsibility (EPR) regimes for plastic and e-waste, where compliance is no longer validated through periodic site inspections alone, but through continuous, invoice-level digital proof submitted via centralized national portals.

While the policy intent of this shift is robust and environmentally necessary, this paper identifies a critical structural risk: the emergence of a “Digital Compliance Cliff” for Micro, Small, and Medium Enterprises (MSMEs. This cliff does not arise from regulatory resistance or environmental negligence, but from a widening digital capability mismatch between large enterprises and smaller manufacturers.

Large corporations typically operate integrated Enterprise Resource Planning (ERP) systems that allow automated data flows from procurement and production records directly into government portals. MSMEs, by contrast, operate in largely manual environments-relying on Excel-based records, fragmented vendor documentation, and informal supply chains. When subjected to the same portal-level validation requirements, these firms face disproportionately high compliance friction.

Analysis of parliamentary disclosures, Central Pollution Control Board (CPCB) portal data, and oversight observations from the Comptroller and Auditor General (CAG) reveals a recurring pattern: registration intent among smaller entities is high, but successful completion of annual digital reporting cycles lags significantly. This “filing gap” suggests that the primary barrier is not awareness or willingness, but technical execution.

The 2025 traceability mandates-particularly requirements for end-to-end invoice linkage and proof of recycled content-intensify this challenge. Tier-2 and Tier-3 suppliers, many of whom operate outside formal digital accounting systems, are often unable to generate the standardized data required by centralized portals. As a result, compliance bottlenecks propagate upstream, affecting even larger Brand Owners (PIBOs) that depend on these suppliers.

This paper argues that without tiered digital reporting pathways, analogous to the GST Composition Scheme, the current enforcement architecture risks creating perverse outcomes. These include increased consultant dependency, exclusion of smaller vendors from formal supply chains, and incentives for marginal manufacturers to exit formal branding altogether-outcomes that ultimately undermine the objective of traceability.

The paper concludes that environmental compliance in its current form is increasingly a data systems problem rather than a purely legal or engineering challenge. Bridging this gap requires policy recognition of simplified reporting tiers and the development of compliant digital intermediary infrastructure capable of translating MSME operational data into portal-ready formats.

Plastic Waste Management Rules (2022) - A Practical Guide for Indian Factories by EHSShala

1. Introduction: From Physical Bans to Digital Proof

For much of the last decade, environmental enforcement in India was defined by physical interventions. Regulatory focus between 2016 and 2022 centered on material restrictions-such as plastic thickness bans-and on-site inspections that evaluated installed pollution control equipment, waste storage practices, and physical documentation.

This paradigm began to shift decisively after 2023. Rather than asking whether waste was treated or recycled, regulators increasingly began asking whether these activities could be proven digitally. The introduction and expansion of centralized EPR portals marked a move toward continuous, transaction-level verification. Compliance became less about the presence of infrastructure and more about the integrity of data trails.

A persistent misconception remains within much of Indian industry that environmental compliance is primarily a matter of installing control devices-filters, effluent treatment plants, or waste storage systems. While these remain essential, they are no longer sufficient. Under current regimes, compliance is validated only when physical actions are digitally mirrored, authenticated, and reconciled within government systems.

This shift represents a fundamental change in enforcement logic. Environmental compliance has transitioned from a periodic, inspector-driven process to an always-on, algorithmically validated one. Understanding the implications of this transition-particularly for MSMEs operating at the margins of digital readiness-is essential to ensuring that regulatory objectives are achieved without unintended economic exclusion.

2. The Regulatory Shift: “Prove It Digitally”

2.1 How the Centralized EPR Portal Operates

The Centralized Extended Producer Responsibility (EPR) Portal administered by the Central Pollution Control Board (CPCB) represents a structural redesign of environmental enforcement. Rather than functioning as a passive filing repository, the portal operates as a transaction-validation system.

At a simplified level, the system requires the following sequence:

- Registration of Producers, Importers, and Brand Owners (PIBOs)

- Declaration of material placed in the market (plastic packaging, electrical equipment, etc.)

- Procurement of EPR certificates from registered recyclers or processors

- Annual return filing, reconciling material introduced with material recycled

- Audit and verification, including invoice matching and quantity reconciliation

Each step is digitally interlinked. A downstream failure-such as a recycler’s invoice mismatch or delayed upload-invalidates the upstream entity’s compliance record. In effect, compliance is no longer evaluated entity-by-entity, but network-by-network.

This design reflects a deliberate policy choice: shifting enforcement away from episodic inspections toward continuous digital traceability.

2.2 The 2025 Traceability Mandate

The 2025 phase of EPR implementation introduces a critical escalation: end-to-end traceability.

Under current mandates, it is no longer sufficient for a PIBO to declare that waste has been recycled. The entity must digitally demonstrate:

- A verifiable linkage between material introduced and material recycled

- Recycler-specific invoices mapped to declared quantities

- Temporal alignment between production, sale, collection, and recycling

- In certain categories, proof of recycled content incorporation (e.g., minimum percentage of recycled plastic in packaging)

This requirement fundamentally alters the nature of compliance. Environmental responsibility is now enforced through data lineage, not just outcomes.

For large enterprises with integrated procurement, inventory, and accounting systems, these requirements can be operationalized through automated workflows. For smaller entities, particularly those embedded in informal or semi-formal supply chains, the same requirements represent a structural hurdle.

2.3 Why MSMEs Are Structurally Exposed

MSMEs typically operate with three characteristics that clash with portal-based enforcement:

- Fragmented supply chains, often involving unorganized or semi-organized vendors

- Manual recordkeeping, centered around Excel sheets and paper invoices

- Limited internal compliance capacity, with EHS responsibilities handled part-time

When subjected to invoice-level traceability mandates, these characteristics create compounding friction. A single missing or non-standard invoice from a Tier-2 supplier can cascade into non-compliance for the brand owner.

This exposure is not a result of regulatory avoidance. Rather, it reflects a misalignment between operational reality and digital validation logic.

3. The Digital Divide: Evidence of the Compliance Cliff

3.1 The Filing Gap (Official Disclosures)

Parliamentary disclosures and CPCB reporting indicate a recurring pattern across states: the number of registered PIBOs consistently exceeds the number of entities that successfully complete annual return filings.

For example, responses to Lok Sabha Unstarred Question No. 2136 (December 9, 2024) highlighted state-level discrepancies between registered entities and completed filings under EPR regimes. While registrations increased steadily, a significant subset of entities failed to conclude the reporting cycle for the relevant financial year.

This divergence-referred to in this paper as the “filing gap”-is a critical indicator. It suggests that awareness and intent are not the primary constraints. Instead, the bottleneck appears during the technical execution phase of compliance.

3.2 Digital Hardening and Its Side Effects

In parallel, regulatory scrutiny has intensified. Lok Sabha Unstarred Question No. 2193 (December 9, 2024) confirmed that CPCB audits uncovered irregularities, including the issuance of fraudulent EPR certificates. In response, regulators appropriately tightened portal security and verification protocols.

These measures-such as enhanced authentication requirements, stricter validations, and audit trails-were necessary to preserve system integrity. However, they also increased the digital hardness of the compliance process.

For MSMEs without dedicated compliance or IT personnel, managing frequent password resets, multi-factor authentication, document re-uploads, and validation errors has become a non-trivial operational burden. The same controls that improve enforcement reliability can inadvertently widen capability gaps.

3.3 Infrastructure Readiness at the Ground Level

Observations from the Comptroller and Auditor General (CAG), including findings from the Performance Audit on Waste Management (Report No. 2 of 2024), consistently highlight deficiencies in systematic data collection at the local level. Urban Local Bodies (ULBs), recyclers, and small operators often lack standardized procedures for recording, aggregating, and reporting waste flows.

This lack of structured data at the point of generation makes downstream digital mirroring difficult. Portal-level traceability assumes the existence of clean, standardized inputs-an assumption that does not uniformly hold across MSME ecosystems.

Taken together, these indicators reveal the contours of the Digital Compliance Cliff: a point at which regulatory intent, technological enforcement, and enterprise capability diverge sharply.

4. Cost vs Capacity: The Regressive Nature of Digital Compliance

4.1 Excel vs API: A Structural Comparison

At the core of the Digital Compliance Cliff lies a fundamental asymmetry in how enterprises interact with compliance systems.

Large enterprises typically operate integrated digital stacks. Procurement orders, material inward records, production data, and sales invoices are captured within ERP systems. When environmental reporting obligations arise, data can be programmatically extracted, validated, and transmitted to government portals with minimal manual intervention.

MSMEs operate in a materially different environment. Compliance data is usually maintained through:

- Spreadsheet-based registers

- Physical invoices and challans

- Vendor declarations received in non-standard formats

Under portal-based enforcement, these manual systems are required to interface with algorithmic validation engines designed for structured, standardized inputs. The result is a high frequency of mismatches-quantity deviations, date inconsistencies, format errors-that trigger portal rejections.

This mismatch is not a question of diligence, but of system design compatibility.

4.2 Cost of Compliance as a Percentage of Revenue

The economic impact of this mismatch becomes evident when compliance costs are viewed relative to enterprise scale.

For large corporations, digital compliance costs-ERP configuration, consultant support, audit processes-represent a negligible fraction of turnover. These costs are amortized across large volumes and embedded within existing systems.

For micro and small enterprises, the same compliance obligations translate into:

- Recurring consultant fees for portal management

- Time diverted from core operations to resolve portal errors

- Purchase of EPR credits at market prices without bargaining power

When expressed as a percentage of revenue, the compliance cost curve becomes regressive: smaller entities incur disproportionately higher costs for each unit of material placed in the market, despite having a significantly smaller environmental footprint.

This asymmetry is central to understanding why uniform digital enforcement can produce unequal economic outcomes.

4.3 The Consultant Dependency Trap

A notable consequence of portal complexity has been the emergence of consultant-led compliance execution.

In theory, consultants are meant to advise, interpret regulations, and build internal capability. In practice, many MSMEs now rely on third parties for:

- Portal logins

- Data uploads

- Error resolution

- Annual return submission

Compliance becomes a transactional service rather than an institutional function. Over time, this dependency erodes internal understanding and resilience. When consultants disengage or errors occur, enterprises find themselves unable to diagnose or correct compliance failures independently.

This dynamic creates a fragile compliance ecosystem-one that is operationally compliant on paper but structurally vulnerable.

5. Emerging Behavioral Consequences: Early Signals from the Field

While long-term outcomes of digital enforcement will emerge over time, early behavioral patterns are already observable across MSME ecosystems.

5.1 Formal Exit Risk

One emerging response to digital friction is a reduction in formal branding. By selling products in unbranded or loosely labeled forms, marginal manufacturers can avoid classification as Brand Owners, thereby exiting EPR obligations altogether.

This response does not eliminate environmental impact. It merely shifts activity outside the traceable perimeter-counter to the objectives of the EPR framework.

5.2 Supply Chain Exclusion

Large Brand Owners, facing strict validation requirements, are increasingly screening vendors based on data readiness rather than operational competence alone. MSMEs unable to provide standardized digital documentation risk exclusion from formal supply chains.

This creates a feedback loop: enterprises most in need of digital transition support are the first to be excluded, accelerating market consolidation rather than inclusive compliance.

5.3 Compliance Outsourcing Without Capability Building

A third pattern is the outsourcing of compliance as a black-box function. While this may achieve short-term filing success, it prevents learning and adaptation. Over time, enterprises remain dependent on external actors without developing internal data discipline.

These behavioral shifts are not speculative. They are rational responses to friction within the system. However, if left unaddressed, they risk undermining both environmental traceability and MSME sustainability.

6. Clarifying the Scope: What This Paper Does NOT Argue

Given the sensitivity of environmental regulation and the legitimate urgency of waste management reform, it is necessary to clearly define the boundaries of this analysis.

This paper does not argue that:

- Environmental traceability requirements should be diluted or rolled back

- MSMEs should be exempt from environmental responsibility

- Digital enforcement mechanisms are inherently flawed or unnecessary

Nor does it suggest a return to inspection-only enforcement models.

Instead, this paper argues that uniform digital enforcement without tiered execution pathways risks producing exclusionary outcomes. When compliance systems assume a level of digital maturity that does not exist uniformly across enterprise classes, enforcement effectiveness may increase on paper while real-world traceability weakens.

The intent of this clarification is not defensive, but constructive: to ensure that environmental objectives are achieved through usable, scalable systems, rather than through compliance structures that inadvertently privilege scale over substance.

7. Bridging the Gap: Policy and System-Level Recommendations

7.1 Tiered Digital Reporting for MSMEs

A practical policy response to the Digital Compliance Cliff is the introduction of simplified digital reporting tiers for MSMEs, calibrated to turnover and material volume.

India already operates such a model successfully through the GST Composition Scheme, which recognizes that uniform procedural requirements impose unequal burdens on small enterprises. A similar logic can be applied to EPR reporting, where:

- Core environmental accountability is retained

- Reporting granularity is adjusted to execution capacity

- Progressive transition pathways are clearly defined

Such an approach would preserve regulatory intent while reducing unintended exclusion.

7.2 Recognition of Digital Intermediary Infrastructure

The current enforcement architecture implicitly assumes that every regulated entity can directly interface with government portals. This assumption does not reflect ground realities.

A more resilient model would formally recognize digital compliance intermediaries-platforms that can:

- Translate MSME operational data into standardized portal-ready formats

- Maintain audit trails and validation logic

- Reduce manual error rates while preserving data integrity

These intermediaries should be viewed as compliance infrastructure, not as circumvention mechanisms. Their role would be analogous to GST Suvidha Providers (GSPs) in the taxation ecosystem.

7.3 Reframing Compliance as a Data Systems Challenge

At its core, the Digital Compliance Cliff is not a legal failure or an enforcement failure. It is a data systems mismatch.

Environmental enforcement has become algorithmic. Without corresponding investment in data capture, standardization, and translation at the MSME level, regulatory ambition risks outpacing execution capacity. Aligning enforcement design with enterprise reality is therefore a prerequisite for sustainable compliance outcomes.

8. Conclusion: Environmental Compliance as a Data Problem

India’s transition toward digital, traceability-driven environmental enforcement is both necessary and inevitable. The scale and complexity of modern waste streams demand systems that are transparent, auditable, and resistant to manipulation.

However, enforcement strength must be matched with infrastructure inclusivity. When compliance systems become inaccessible to smaller enterprises-not by intent, but by design-the result is not improved environmental outcomes, but behavioral adaptation that circumvents traceability altogether.

This paper concludes that environmental compliance in its current phase must be treated primarily as a data engineering and systems design challenge, not merely as a regulatory obligation. Bridging the Digital Compliance Cliff is essential to ensuring that India’s environmental goals are met without eroding the economic base of its MSME sector.

Methodology and Disclosure

Methodology:

This paper employs a data triangulation approach combining:

- Analysis of parliamentary disclosures (Lok Sabha responses, 2024–2025)

- Review of public metrics and operational structures of the CPCB EPR Portal

- Observations from CAG performance audits related to waste management systems

- Aggregated, anonymized market intelligence derived from engagement with MSMEs

Limitations:

The analysis focuses on plastic and e-waste EPR regimes as representative digital compliance systems. Findings may not generalize uniformly across all environmental regulations.

Disclosure:

The author is the founder of EHSSaral, a platform working on environmental compliance digitization. References to digital intermediary systems are presented in a category-level context, not as product endorsement.

About the Author

Harshal T Gajare is an environmental systems analyst and founder of EHSSaral, an environmental compliance infrastructure initiative focused on simplifying regulatory execution for Indian MSMEs. With field exposure to environmental monitoring and compliance workflows, his work focuses on the intersection of regulation, data systems, and enterprise capability.

References

All sources cited are publicly available government disclosures, statutory reports, or official regulatory portals.

Government & Parliamentary Sources

- Lok Sabha Unstarred Question No. 2136

Status of EPR Compliance and Filing under Plastic Waste Management Rules

Ministry of Environment, Forest and Climate Change (MoEFCC)

Answer dated: 9 December 2024 - Lok Sabha Unstarred Question No. 2193

Irregularities in EPR Certificates and Action Taken by CPCB

Ministry of Environment, Forest and Climate Change (MoEFCC)

Answer dated: 9 December 2024 - Central Pollution Control Board (CPCB)

Guidelines on Extended Producer Responsibility for Plastic Packaging

Issued under Plastic Waste Management Rules (as amended)

Available via: Centralized EPR Portal documentation

Audit & Oversight Reports

- Comptroller and Auditor General of India (CAG)

Performance Audit on Waste Management

Report No. 2 of 2024

Government of India

Regulatory Frameworks & Portals

- Centralized EPR Portal – CPCB

Portal structure, registration workflows, filing requirements, and public dashboards

(Plastic Waste and E-Waste EPR Modules) - Plastic Waste Management Rules, 2016

Including subsequent amendments up to 2024–2025 - E-Waste (Management) Rules, 2022

Including implementation guidelines and compliance obligations

Policy Analogies & Comparative Frameworks

- Goods and Services Tax (GST) Council

Composition Scheme Framework for MSMEs

Government of India

(Used as an analogy for tiered compliance design)

Field & Market Intelligence

- Aggregated MSME Compliance Observations (2023–2025)

Anonymized operational insights derived from industry interactions in Maharashtra

(Non-public, summarized for pattern analysis only)

Harshal T Gajare

Founder, EHSSaral

Founder - EHSSaral| Partner - Perfect Pollucon | ISO 14001 Lead Auditor | Second-generation environmental professional simplifying EHS compliance for Indian manufacturers through practical, tech-enabled guidance.

Related Blogs

Chemical Accidents Rules, 1996: A Practical Guide for Indian EHS Officers

Why Good People Still Struggle With Compliance in Indian SMEs | EHSSaral Research

EHSSaral v1.png)

Blue Category MPCB 3-Year Consent Validity for Recyclers (2026) | EHSSaral

Ozone-Depleting Substances Rules, 2000 - A Practical Guide for Indian Industries

SPCB Consent Conditions: Common Compliance Mistakes Explained | EHSSaral

The Groundwater NOC Trap: Why Industrial Renewal Applications Are Rejected (2023–2025)

Why Running Factories Are Getting Closure Notices in 2026 | EHSSaral

Evolution of EHS in India - (Part 2) Post-Bhopal | EHSShala